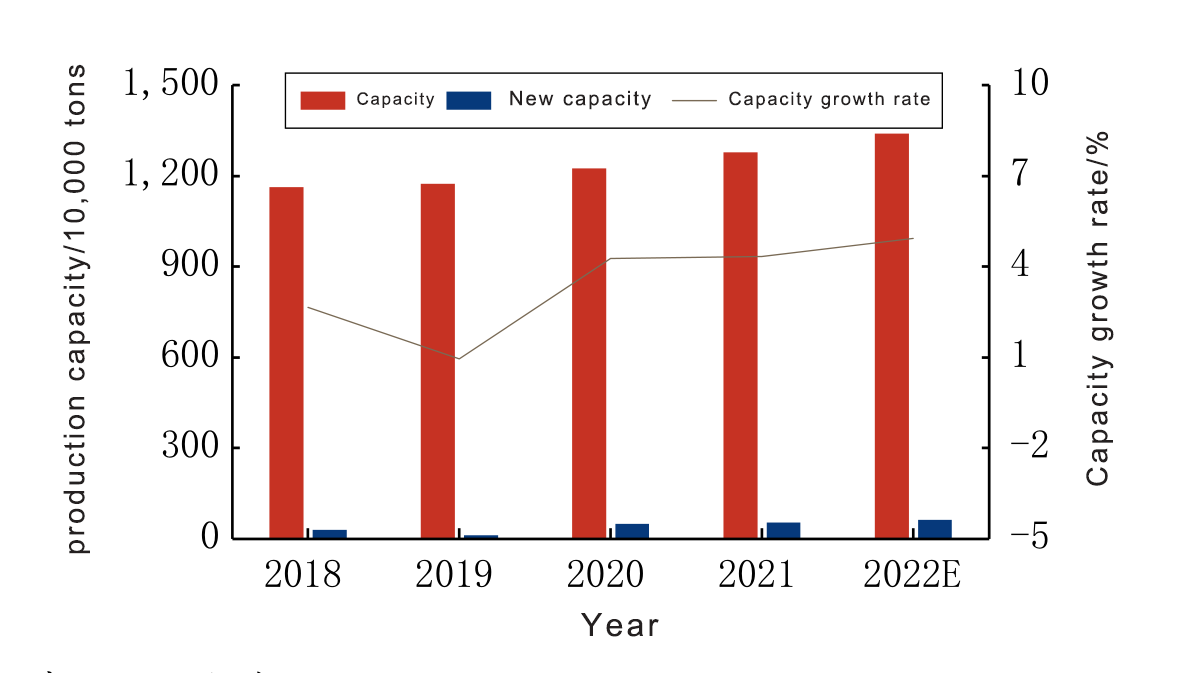

According to statistics, the compound growth rate of offset paper production capacity in China will be 3.9% from 2018 to 2022. In terms of stages, the production capacity of offset paper shows an overall trend of steady increase. From 2018 to 2020, the offset paper industry is in a mature stage, the growth rate of production capacity is not high, the industry’s profitability is gradually shrinking, and the competition in the same industry is intensifying. From 2020 to 2022, the production capacity of offset paper will increase slightly, and most of the new production capacity in the industry is the expansion of production capacity of large-scale paper companies. From July 2021, the “double reduction” policy will be promoted, and the demand for training books will shrink significantly, the balance between supply and demand will decrease, and some planned production capacity will be delayed. Under the influence of the paperless office and the “double reduction” policy, the overall demand for offset paper is “sluggish”, and the price of wood pulp is high, and the industry’s profits are low. The advantages of large-scale paper companies’ integration of forestry, pulp and paper are further reflected. Supported by publishing demand, the demand for offset paper is relatively rigid. In recent years, some large paper companies have further expanded their production capacity; small paper companies are more flexible, and when their profitability is not ideal, they will often switch production or shut down in stages.

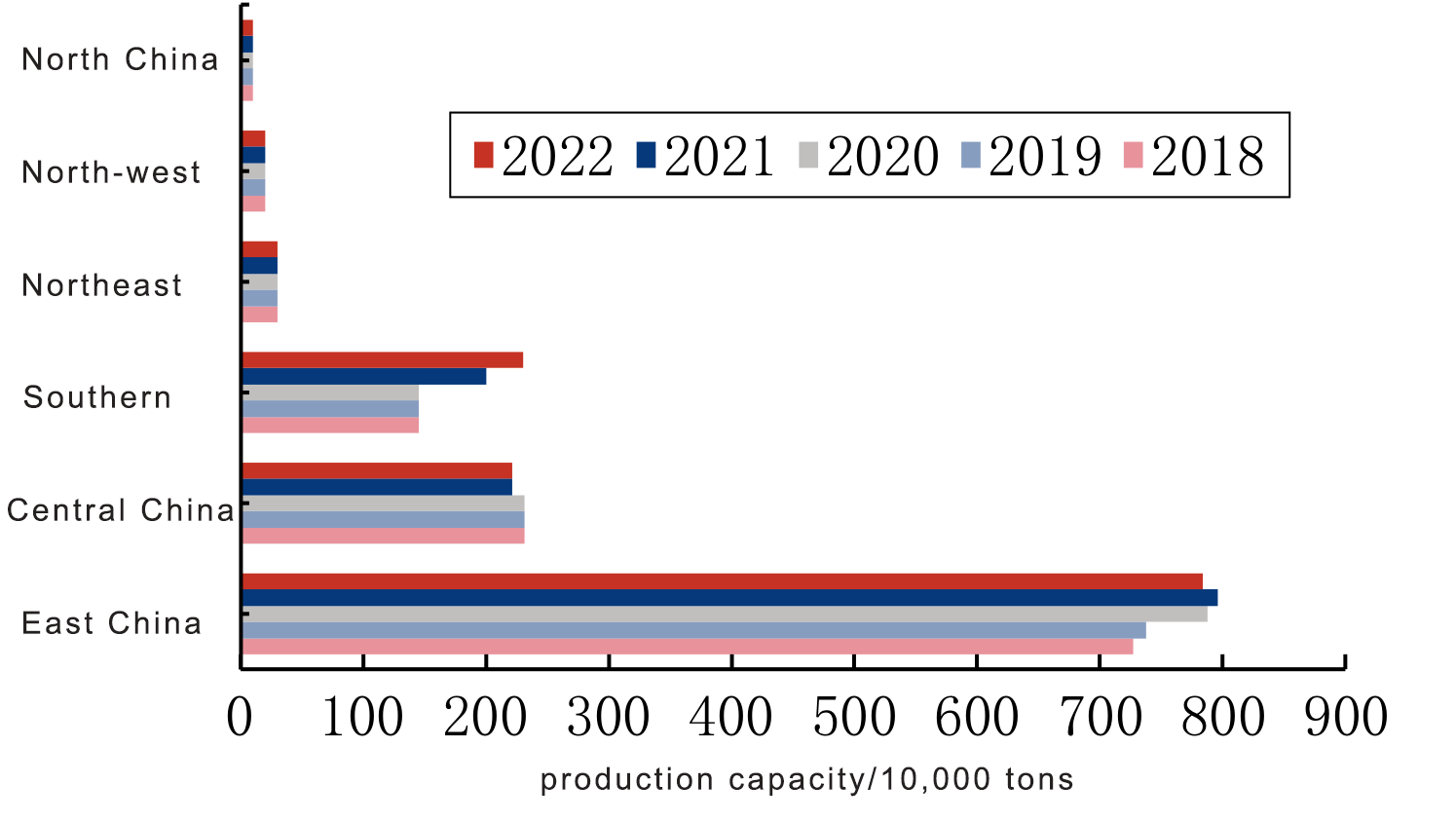

Judging from the changes in the regional distribution of offset paper in China in the past five years, the East China region has always been the main production area for offset paper in China. The proximity to the consumer end and relying on the advantages of raw materials are the main reasons for supporting the concentration of local offset paper production capacity. The production capacity in South China has grown rapidly in recent years, and the planned production capacity in the future is relatively concentrated, mainly because the region is suitable for the integrated development of forestry, pulp and paper. On the whole, the production capacity distribution of offset paper has been diversified in the past five years, but in terms of production capacity, it is still dominated by East China, Central China, and South China, and the production capacity layout in other regions is relatively small.

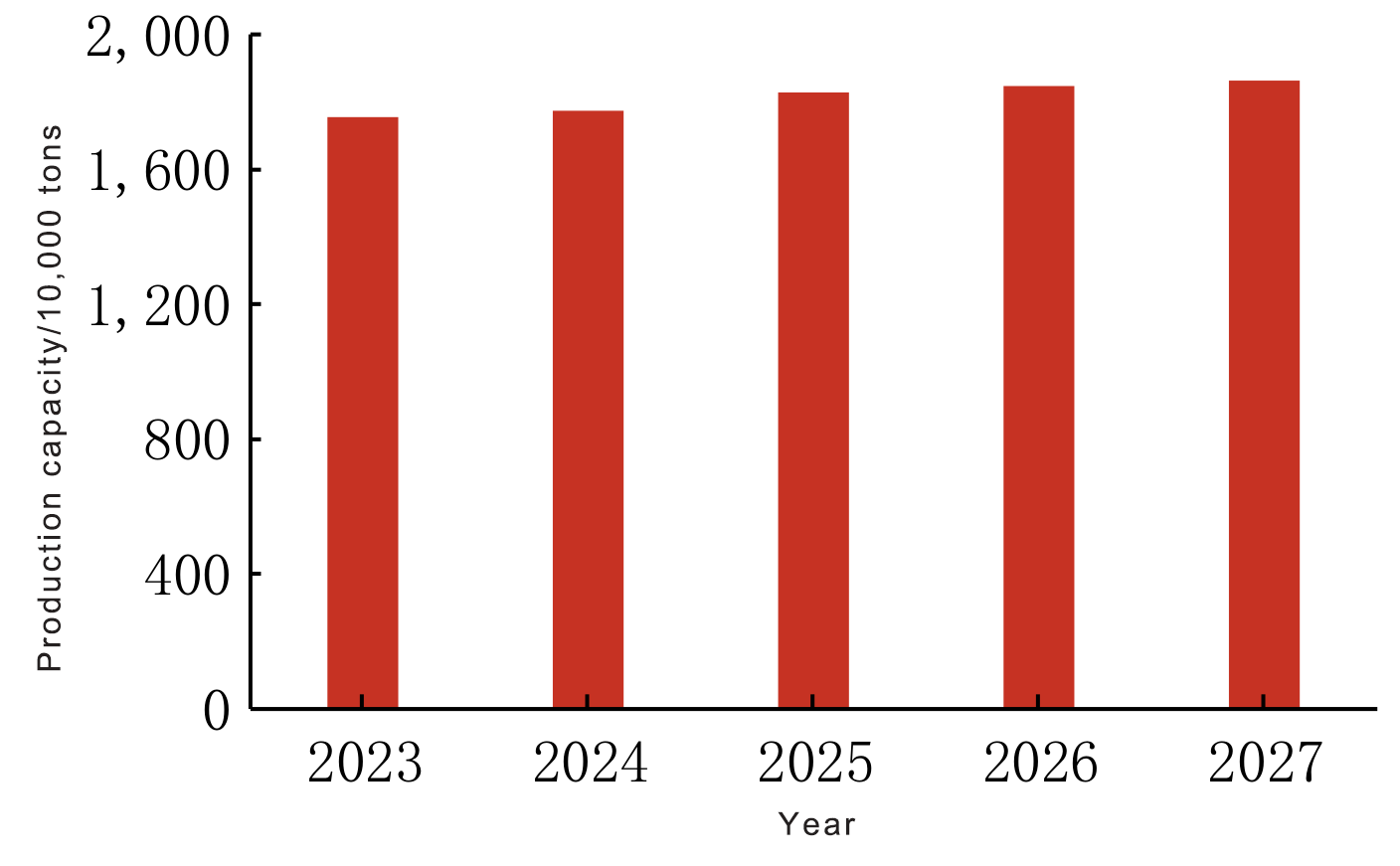

In the next five years, there will be a lot of planned production capacity of offset paper, mostly concentrated in the period from 2023 to 2024. The industry plans to put into production more than 5 million tons, and the production capacity will be concentrated in South China, Central China, East China and other regions. The production capacity of offset paper in China has increased significantly at the same time. It is estimated that the production capacity of offset paper in China will increase by an average of 1.5% from 2023 to 2027. The factors that stimulate new production capacity are, on the one hand, the considerable benefits of the woodfree paper industry in the past few years, which have attracted investment enthusiasm; Under the general trend of further upgrading, industry investment planning has increased and concentrated.

Post time: Jan-09-2023